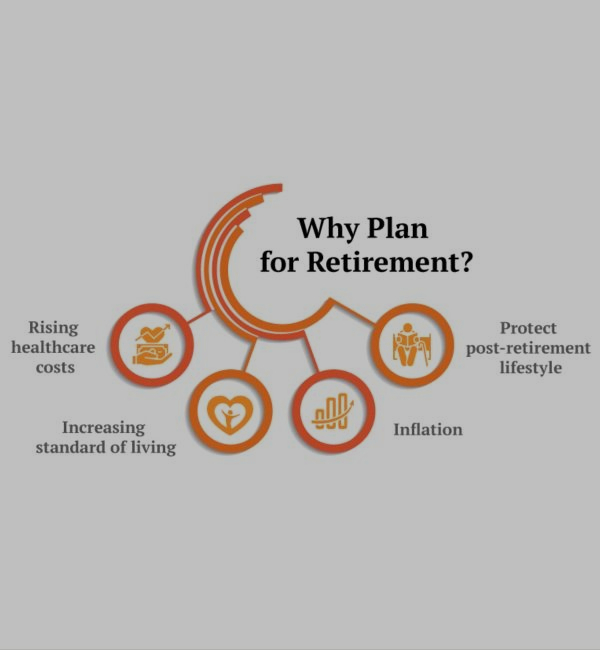

Retirements Plannings

Retirement planning establishes desired levels of retirement income as well as the steps and choices required to get there. Identification of income sources, estimation of expenses, implementation of a savings plan, and management of assets and risk are all components of retirement planning. To determine whether the retirement income objective will be achieved, future cash flows are predicted.

Stages of Retirement Planning:

- Young Adulthood (Age 21-35): Young adults may not have much money available for investing, but they do have time to wait for investments to mature, which is a crucial and priceless component of retirement savings. The idea of compound interest is to responsible for this. The longer you have, the more interest you will be able to earn thanks to compound interest. Because of the wonders of compounding, even if you can only set away 2000₹ per month, starting to invest at age 25 will increase your money's value by three times compared to starting later in life, at age 45. There is no way to make up for lost time, even if you were to invest more money in the future.

- Early Midlife (Age 36-50): Financial burdens including mortgages, student loans, insurance premiums, and credit card debt frequently appear in the early middle age. At this point of retirement preparation, saving must yet continue. These are some of the best years for aggressive saving because of the increased income and the amount of time you still have to invest and earn interest.

- Later Midlife (Age 50-65): Your investment portfolio should grow more conservative as you become older. There are a few benefits even though there isn't much time left to save for individuals who are in this stage of retirement planning. You may have more money available to invest if you earn more money and some of the aforementioned costs (mortgages, school loans, credit card debt, etc.) have already been paid off by this point.